MARKET DEVELOPMENT – GBP DROPS AS LABOUR LEADER STEPS UP ELECTION TALK

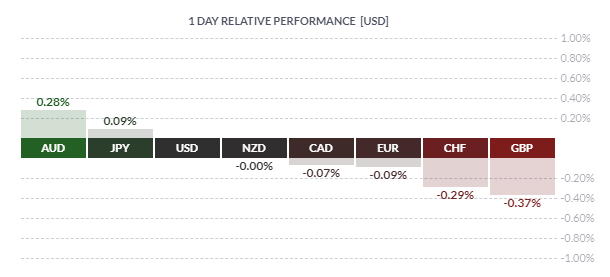

USD: After yesterday saw the largest daily drop since November, the USD is clawing back some losses. Risks continue to remain tilted to the downside for the greenback as the Fed-induced USD strength unwinds amid the central banks dovish tilt. Comments from Fed’s Bostic who open up the possibility of a rate cut, suggest that the near-term outlook for rates will be to wait and see the incoming data. Market attention will be placed on Fed’s Powell and Clarida scheduled to speak late. However, it is unlikely Powell will deviate from his views presented last week. Q1 outlook for USD.

GBP: Having failed to make a firm break above the 1.28 handle, the Pound is underperforming this morning. Yesterday saw PM May defeated for the second time in as many days in which the Dominic Grieve amendment had been approved. Consequently, this means that PM May must provide a plan B in 3 days as opposed to 21 days if her deal fails. Elsewhere, GBP had taken a fresh leg lower this morning after UK Labour Leader Corbyn stepped up talk for a general election over a second referendum if PM May’s deal fails. As it stands, Theresa May’s deal has a very slim chance of passing.

AUD: Marginal outperformance in the Aussie, despite some rather disappointing Chinese Inflation data overnight. Much of the support had stemmed from cross buying via AUDNZD, which in turn seen the Aussie make a move towards the 50 and 100DMA situated at 0.7187 and 0.7177 respectively. However, selling interest could reassert itself once 0.7200 is hit, particularly given that the so-called US-China trade optimism has yet to yield much significant progress.

Economic Calendar: Thursday, January 10, 2019 – North American Releases

Webinar Calendar: Thursday, January 10, 2019

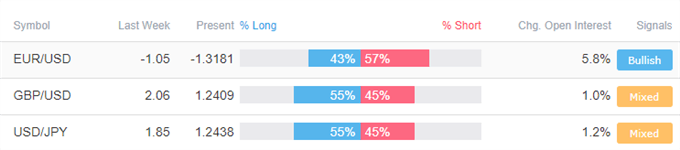

Client Sentiment

No comments:

Post a Comment