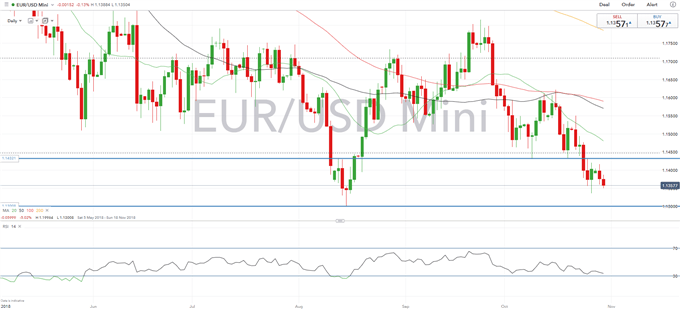

Bitcoin (BTC), Ethereum (ETH), Ripple (XRP): Prices, Charts and News

- UK Cryptoasset Taskforce warns of ‘substantial potential risks’.

- Cryptocurrencies fade lower in thin market conditions.

UK REGULATOR RELEASES CRYPTOASSET UPDATE

The UKCryptoasset Taskforce -consisting of HM Treasury, the Financial Condust Authority (FCA) and the Bank of England – has released a paper warning that there are ‘substantial potential risks associated with cryptoassets, and the most immediate priorities for the authorities are to mitigate the risks to consumers and market integrity and prevent the use of cryptoassets for illicit activity'. The report concludes that strong action should be taken ' to address the risks associated with cryptoassets that fall within existing regulatory frameworks’.

The report adds that the authorities will consult on, among other areas,

‘a potential prohibition of the sale to retail consumers of derivatives referencing certain types of cryptoassets (for example, exchange tokens), including CFDs, options, futures and transferable securities’.

Market reaction to the report saw cryptocurrencies shed 3%-5%, pushing some coins back to noted support levels and the overall market capitalization to just above $200 billion, a six-week low. The cryptocurrency market has traded in a tight range over the last few weeks and volume remains low.

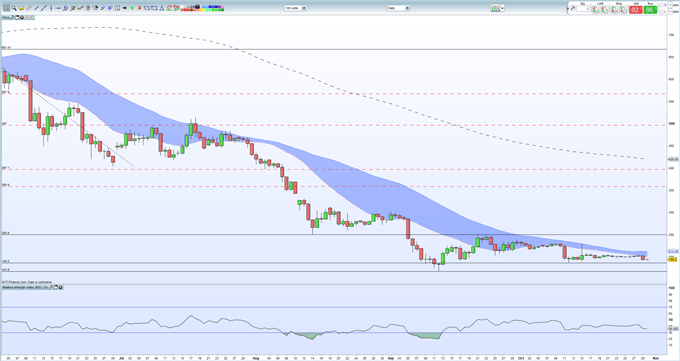

Bitcoin (BTC) currently trades around $6,250, just above horizontal support at $6,110, a break of which would open the way back to the August 15 low at $5,887. Bitcoin is below all three moving averages.

BITCOIN (BTC) DAILY PRICE CHART (JUNE – OCTOBER 30, 2018)

Ethereum (ETH) is back below $200, and all three moving averages, and is eyeing support at $186.5 ahead of $167.6.

ETHEREUM (ETH) DAILY PRICE CHART (JUNE – OCTOBER 30, 2018)

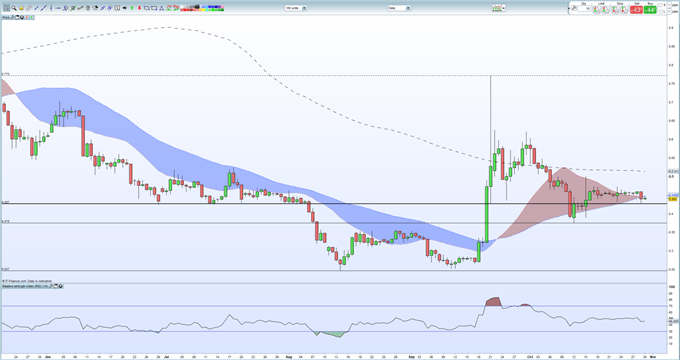

Ripple (XRP) is not immune to the sell-off and trades around $0.44, sharply lower than the September 21 ‘spike-high’ of $0.77. Support is seen at $0.427 ahead of $0.375. Ripple also trades below all three moving averages.

RIPPLE (XRP) DAILY PRICE CHART (JUNE – OCTOBER 30, 2018)