Talking Points:

- The US Dollar is having an atypical month of October, usually one of its best months of the year. The recent move lower by the DXY Index could be the greenback recoupling with Fed rate expectations.

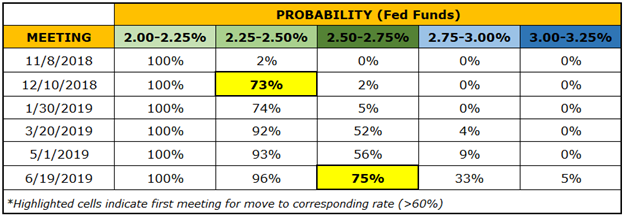

- A 25-bps hike is being priced-in for December 2018, but then no rate move is anticipated until at least June 2019.

The US Dollar finds itself struggling in the second half of October. The turn lower over the past week may be seen as a surprise to some, given the historical performance of the greenback at the start of the fourth quarter. Over the past 10-years, October has been the third best month of the year for the DXY Index, gaining on average +0.89%. Yet in October 2018, the DXY Index is only up by +0.1%, having erased -1.18% from its high set just earlier this week.

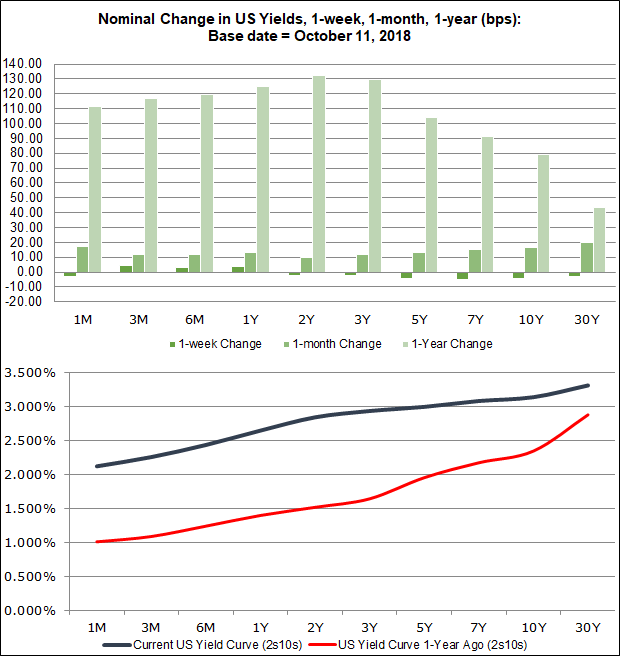

The lack of US Dollar upside is surprising for several reasons, perhaps most notably because of what has happened with US Treasury yields in recent weeks. Not only have yields picked up across the curve over the past month, they gains have reinforced the predominant trend over the past year, which has been gains in the short-end of the curve.

US Treasury Yield Curve Chart: Change Over 1-week, 1-month, and 1-year (Chart 1)

Yet during this time period, as we’ve seen yields firm up, Fed rate hike odds haven’t moved much at all. Indeed, the lack of significant momentum higher in Fed rate expectations may be part of the reason why the US Dollar’s initial October rally was checked, and why over the past week the US Treasury yield curve has flattened out slightly. To wit: prior to the September FOMC meeting, there was a 78% chance of a 25-bps rate hike in December 2018 and a 51% chance of another hike in March 2019. Now, these odds have shifted to 73% and 52%, respectively.

Federal Reserve Rate Hike Expectations (October 11, 2018) (Table 1)

Earlier this week, we argued that “it's atypical for the US Dollar to gain while the Fed's glide path is flattening and pricing out rate hikes, which leads us to the necessary conclusion that US Dollar gains are solely due to the weakness seen by the largest component of the DXY Index, the Euro (57.6% weight).” It would appear then that US Dollar in losses in recent days are tied to the flattening of the US Treasury yield curve over the past week and a recoupling to otherwise docile Fed fund rate expectations over the past month.

DXY Index Price Chart: Daily Timeframe (January to September 2018) (Chart 2)

No comments:

Post a Comment